The United Arab Emirates (UAE) has sent a thunderous message to the global financial community. In a massive enforcement sweep during 2025, regulatory authorities imposed a staggering AED 339 million in fines across a broad spectrum of the financial sector, including banks, exchange houses, and insurance providers. This crackdown isn’t just a headline—it is a paradigm shift in how business is conducted in the Middle East.

Stay compliant with UAE AML laws after the AED 339M crackdown. A Comprehensive Guide for Businesses covering key risks, penalties, and strategies to avoid costly fines and ensure compliance.

For business owners and corporate entities operating within the UAE or planning to enter the market, the landscape has changed. Compliance is no longer a “check-the-box” exercise; it is the cornerstone of operational survival. To navigate these turbulent regulatory waters, communicating and coordinating with MCS (Offshore Company Specialist) corporate services is the most effective way to ensure your business remains on the right side of the law.

The Significance of the AED 339 Million Enforcement

The sheer scale of these penalties—totaling AED 339 million—reflects the UAE’s zero-tolerance policy regarding Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF). Historically, many viewed the UAE as a more flexible jurisdiction, but the recent alignment with Financial Action Task Force (FATF) recommendations has brought the country’s standards in line with the strictest global regimes.

This crackdown specifically targets sectors that were previously under less scrutiny. While banks have always been the primary focus of AML efforts, the current wave of fines hit exchange houses and insurers with equal force. This suggests that every financial intermediary is now under the microscope.

Why Compliance Failures Occurred: The Lessons Learned

The regulatory reports following the fines highlight several recurring failures. Understanding these is vital for any entity wishing to avoid a similar fate.

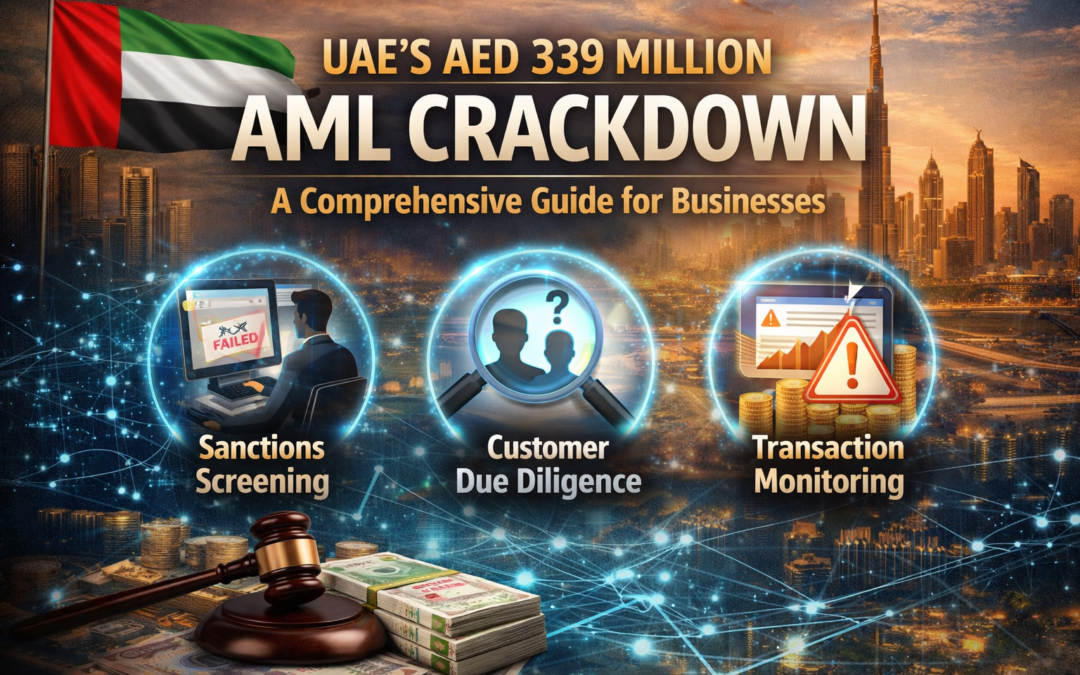

1. Gaps in Sanctions Screening

One of the most common pitfalls was the failure to properly screen clients against international and local watchlists. In some cases, businesses were using outdated databases or generic screening tools that failed to flag designated entities. In the fast-moving world of global sanctions, even a 24-hour delay in updating a list can lead to a multi-million dirham fine.

2. Weak Customer Due Diligence (CDD)

Regulators found that many institutions possessed outdated or incomplete information regarding Beneficial Ownership (UBO). Knowing who actually owns and controls a company is a fundamental requirement. Failure to identify the ultimate human being behind a corporate shell is now considered a high-risk compliance breach.

3. Inadequate Transaction Monitoring

Standard, “one-size-fits-all” monitoring rules are no longer acceptable. The crackdown revealed that many firms were using generic thresholds that failed to trigger alerts for suspicious patterns specific to their industry or client profile.

The Solution: A Risk-Based Approach (RBA)

The UAE authorities are pushing for a “Risk-Based Approach.” This means your compliance efforts must be proportionate to the risks your business faces.

- Risk Profiling: You must assign risk scores based on geography, industry type, and transaction volume.

- Enhanced Due Diligence (EDD): For high-risk clients or Politically Exposed Persons (PEPs), standard ID checks are not enough. You must verify the source of funds and, in some cases, perform on-site visits.

- Continuous Improvement: Compliance is not a static document. It requires constant feedback loops where new enforcement findings—like this AED 339 million crackdown—are used to update internal policies.

Why Coordination with MCS is Your Best Strategy

The complexity of these new regulations can be overwhelming for a standard business owner. This is where MCS (Offshore Company Specialist) becomes your most valuable asset.

Rather than trying to build a compliance department from scratch, coordinating with MCS allows you to leverage expert corporate services that are already optimized for the UAE’s rigorous standards. MCS provides the necessary oversight to ensure that your screening scenarios are up-to-date, your UBO documentation is impeccable, and your transaction monitoring is finely tuned.

In an environment where a single mistake can lead to an eight-figure fine, having a professional partner to handle the corporate heavy lifting is not just an advantage—it is a necessity.

Frequently Asked Questions (FAQ)

1. Why did the UAE impose such large fines recently?

The UAE is working to maintain its status as a top-tier global financial hub. By aligning with FATF standards and imposing AED 339 million in fines, they are demonstrating to the international community that they are serious about preventing money laundering and financial crime.

2. Does this crackdown only apply to large banks?

No. The recent enforcement actions hit exchange houses, insurance companies, and other financial intermediaries. Any business that handles financial transactions or provides corporate services is subject to these strict AML laws.

3. What is the most common reason for an AML fine?

The most frequent causes include failing to properly identify the Ultimate Beneficial Owner (UBO), failing to screen clients against current sanction lists, and failing to report suspicious transactions in a timely manner.

4. How can I ensure my business is compliant?

The most effective way is to communicate and coordinate with a professional service provider like MCS. They can perform a compliance audit, identify gaps in your current protocols, and implement the necessary risk-based monitoring systems.

5. What is “Customer Due Diligence” (CDD)?

CDD is the process of collecting and verifying information about a client to ensure they are who they say they are and to assess the risk of doing business with them. This includes identifying the UBO and understanding the nature of the client’s business.

6. Will these regulations make it harder to do business in the UAE?

While the requirements are stricter, they also provide a more stable and reputable environment for legitimate businesses. Companies that prioritize compliance will find it easier to open bank accounts and attract international partners.

7. What are the consequences of non-compliance besides fines?

Beyond the financial penalties, non-compliant firms face “naming and shaming” (public disclosure of the fine), the loss of their operating licenses, and potential criminal prosecution for the company’s directors.

8. How often should I update my AML policies?

In the current climate, your policies should be reviewed at least annually, or immediately following any major regulatory shift or enforcement action by the UAE authorities.

Protect your business and your reputation.

The AED 339 million crackdown is a warning that the “old way” of doing business is over. To ensure your company remains compliant and resilient, visit Offshore Company Specialist (MCS) and let the experts handle your corporate service needs.